- Despite the non-oil revenue surge, debt and subsidy pressures mount

Nigeria is gradually reducing its long-standing dependence on crude oil as a major source of revenue, as non-oil income and tax collection across the country have been on a steady rise, a new report reveals.

The report, titled “Nigeria Unshackled: Inside the Steady Rise of a Fiscal State,” was released by Quartus Economics, an independent economic research and policy think-tank. It examined Nigeria’s economic performance between 2010 and 2025.

The report found that Nigeria has made measurable progress in shifting from an oil-driven economy to one increasingly supported by non-oil revenue, particularly through improved tax collection and fiscal reforms.

From Oil Dependence to Economic Shock

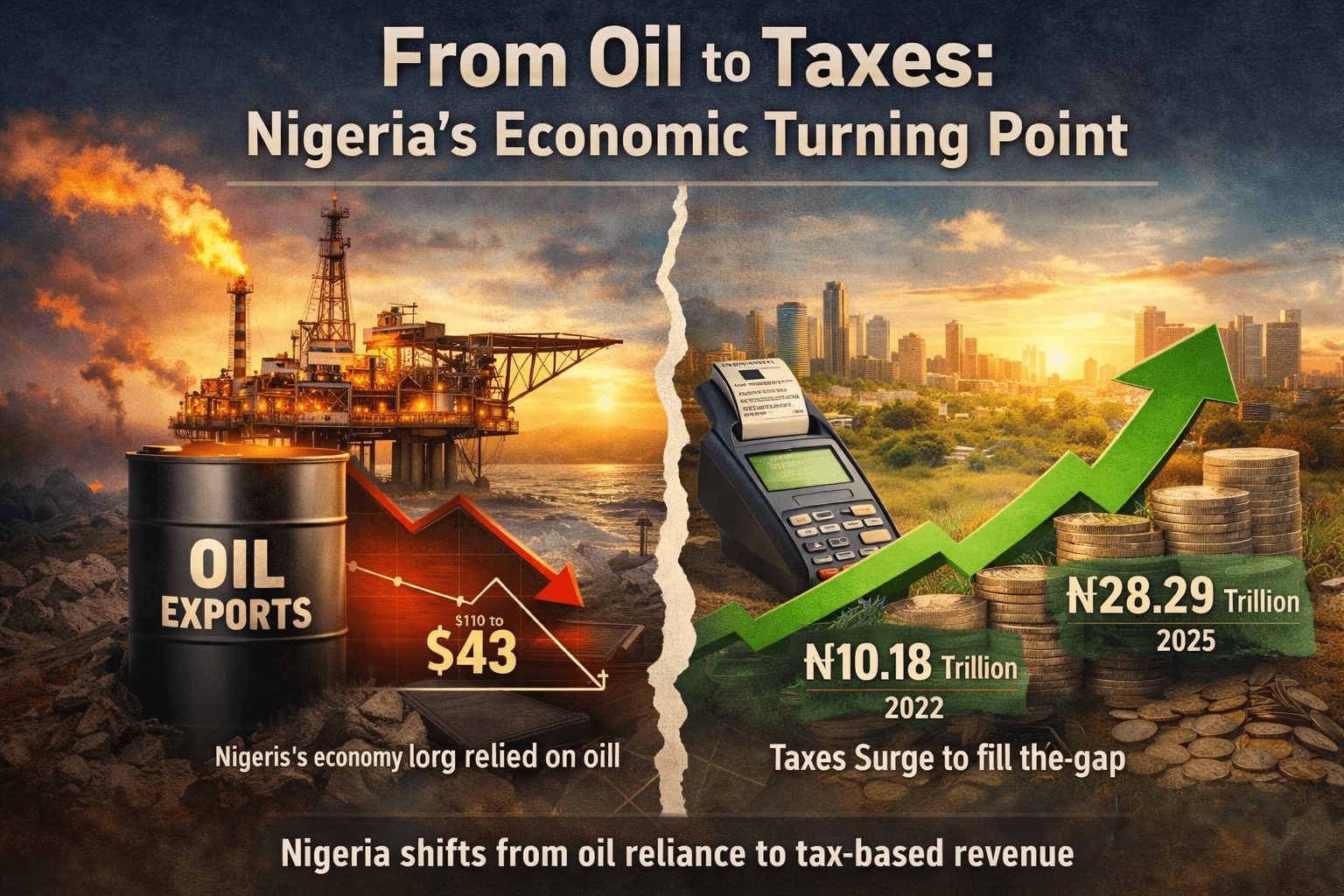

For decades, Nigeria relied heavily on crude oil exports to fund government spending and generate foreign exchange. This made the economy vulnerable to global oil price fluctuations.

The report noted that this structure began to weaken after the sharp decline in oil prices in 2014. The price of crude fell from about $110 per barrel to $43.8 by 2016, triggering a major drop in government revenue.

Between 2015 and 2019, oil revenues fell by 41 per cent compared to the previous five years. As a result, economic growth slowed significantly, dropping to an average of 1.2 per cent annually.

The impact on Nigerians was severe. The report stated that by 2024, income per person had declined, while poverty levels increased across the country.

A Shift Toward Non-Oil Revenue

In response to the crisis, the government intensified efforts to boost revenue through taxation and improved collection systems.

The report described this as a “definitive shift” in Nigeria’s fiscal structure.

It revealed that in 2010, oil accounted for nearly 74 per cent of government revenue. By 2024, that figure had dropped to about 26 per cent.

At the same time, non-oil revenue rose significantly, now contributing nearly 75 per cent of total government income. This marks a major step toward economic diversification.

Tax Revenue on the Rise

One of the most notable developments highlighted in the report is the sharp increase in tax collection.

Tax revenue rose from N10.18 trillion in 2022 to N28.29 trillion in 2025. The report attributed about 86 per cent of this growth to non-oil sectors.

This improvement reflects a combination of policy changes, stricter enforcement, and broader economic activity beyond the oil sector.

The increase in Value Added Tax from 5 per cent to 7.5 per cent also played a role, along with reforms such as centralised revenue collection in the oil sector.

Today, the non-oil sector accounts for more than 70 per cent of total tax revenue, showing clear signs of diversification.

Rising Debt Raises Concerns

Despite these gains, the report warned that Nigeria’s rising debt levels remain a major concern.

The country increased borrowing after the 2014 oil price crash to support spending and fund infrastructure projects.

As a result, Nigeria’s debt-to-GDP ratio rose from about 12 per cent in 2014 to nearly 39 per cent in 2024.

Debt servicing has also become a major burden. In 2012, only about 6 per cent of government revenue went into debt repayment. By 2024, that figure had risen to 38.5 per cent.

The report noted that external debt now makes up a larger share of total debt, partly due to the depreciation of the naira.

However, it added that Nigeria’s debt level remains within acceptable global standards, even though economic growth has not kept pace with the increase in borrowing.

Subsidy Spending Still a Major Drain

The report also highlighted fuel subsidy as a significant strain on public finances.

It is estimated that Nigeria spent about N23.75 trillion on petrol subsidies over a 15-year period. A large portion of this spending occurred between 2021 and 2024.

In 2024 alone, subsidy costs reached N7.1 trillion, making it increasingly unsustainable.

The report described the removal of fuel subsidy as a necessary but difficult reform needed to stabilize public finances and redirect resources to more productive sectors.

READ ALSO:

- Tinubu Approves ₦3.3trn for final settlement of Power Debt

- Outcry as Senate Approves Tinubu’s $6bn Loan in Hours, Debt Set to Hit ₦155trn

- Nigeria Boosts Oil Exports with First Shipping of 950,000 barrels of Cawthorne crude to India

- Nigeria’s Economic Stability Improves in Q1, but Rising Costs Threaten Outlook — CPPE

Looking forward, the report stressed that Nigeria’s transition to a tax-based economy comes with higher expectations from citizens.

As more Nigerians and businesses contribute to government revenue, demand for transparency and accountability will continue to grow.

The report also warned that increased revenue and borrowing must translate into real economic growth and improved living conditions.

It urged the government to invest more in key sectors such as agriculture and manufacturing, which have the potential to create jobs and drive sustainable development.

According to the report, Nigeria must use its borrowing capacity carefully and focus on delivering measurable results for its citizens.

The report concluded that Nigeria has made important progress in reducing its dependence on oil, marking a significant shift in its economic structure.

However, it cautioned that the next challenge lies in ensuring that these gains lead to real improvements in productivity, employment, and living standards.

“Nigeria has broken away from its dependence on oil, but the next challenge is to ensure that this progress leads to real improvements in productivity, employment and living standards.”

For now, Nigeria stands at a critical economic crossroads—one defined by progress, but also by pressing fiscal risks that will shape its future.

Esther Ososanya is an investigative journalist with Pinnacle Daily, reporting across health, business, environment, metro, Fct and crime. Known for her bold, empathetic storytelling, she uncovers hidden truths, challenges broken systems, and gives voice to overlooked Nigerians. Her work drives national conversations and demands accountability one powerful story at a time.