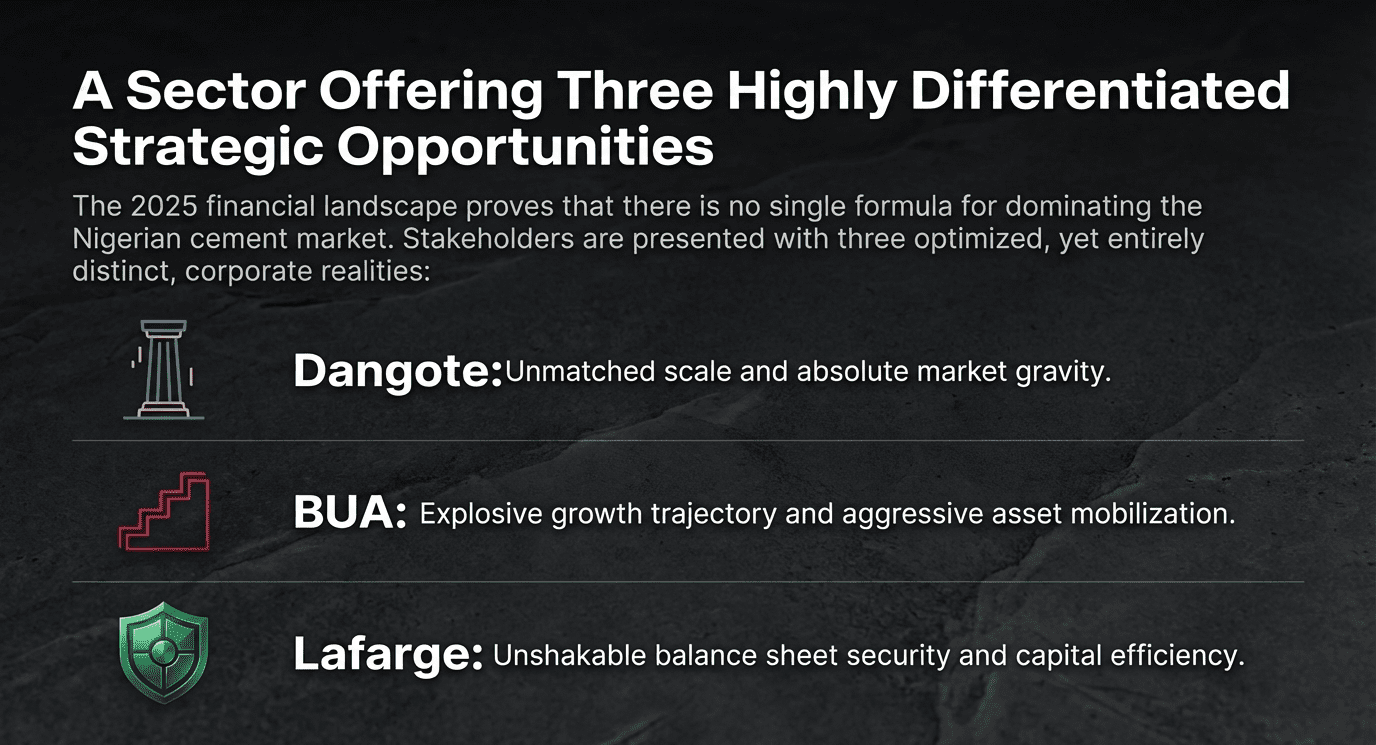

Nigeria’s three major cement producers, Dangote Cement, BUA Cement and Lafarge Africa, posted strong revenue and profit growth in their 2025 audited financial results.

But Dangote Cement stood out by making significantly more profit per bag of cement than its competitors.

The company recorded the highest gross profit margin in the industry, showing it is the most efficient at turning production into profit.

While BUA Cement and Lafarge Africa both crossed the ₦1 trillion revenue mark during the year, Dangote Cement remained far ahead in scale, profitability and market share.

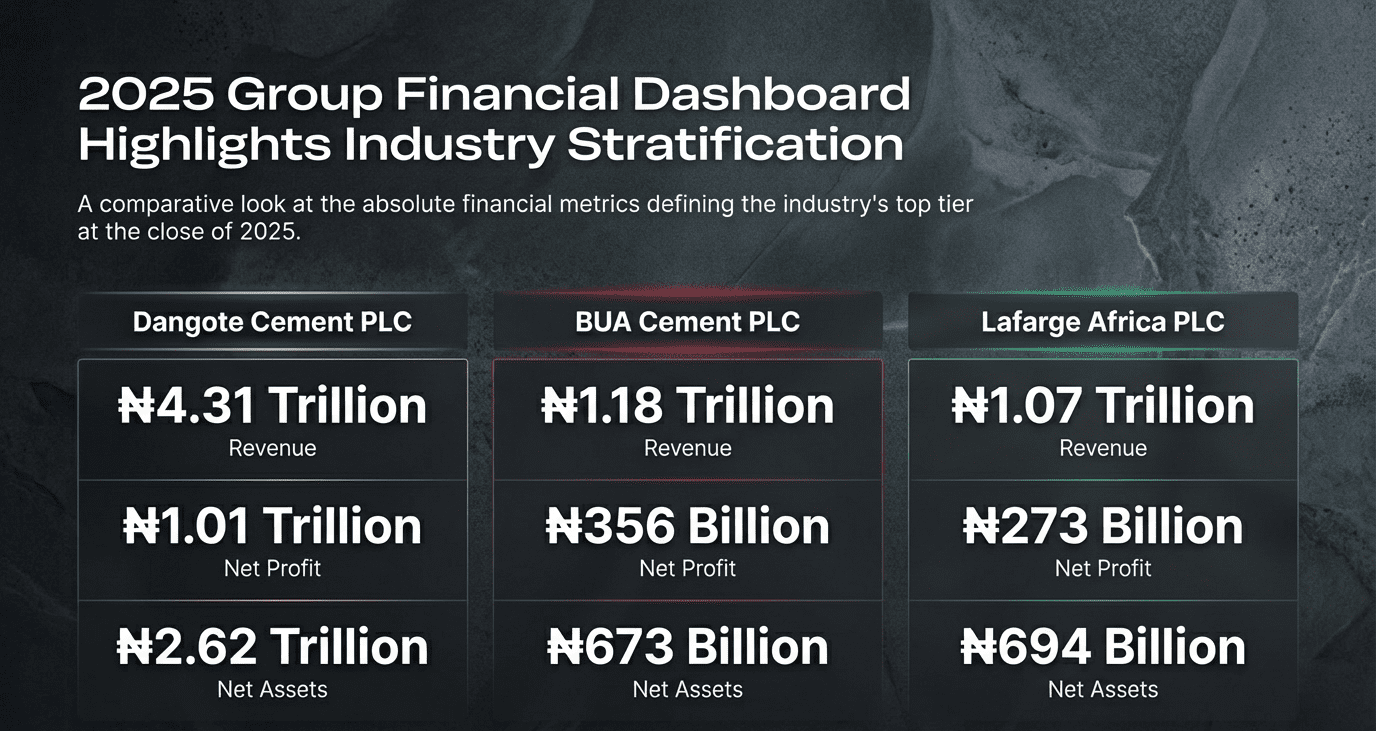

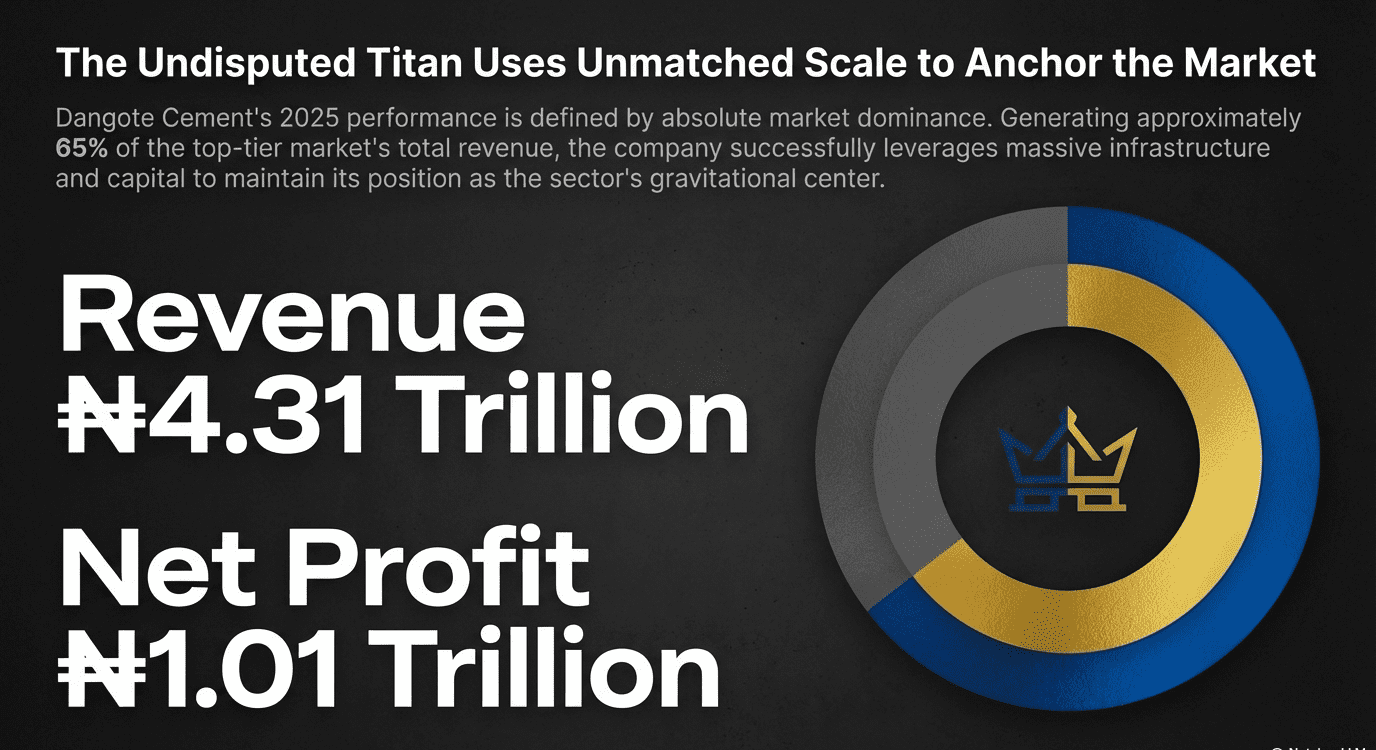

Based on revenue performance, Dangote Cement controlled about 65.7 per cent of the combined market revenue of the three companies, generating ₦4.31 trillion.

BUA Cement accounted for 18 per cent with ₦1.18 trillion, while Lafarge Africa held about 16.3 per cent with ₦1.07 trillion.

Cement giants make over 50k from every ₦1 sale

Dangote Cement posted the highest gross profit margin at 62.05 per cent, meaning it generated more profit from each bag of cement sold than its competitors.

This means that for every ₦1.00 sale, Dangote Cement made over 62 kobo.

The company recorded gross profit of ₦2.67 trillion from revenue of ₦4.31 trillion, maintaining the widest profitability gap in the industry.

READ ALSO:

- How 10 Most Capitalised Stocks Control over 60% of NGX Market Cap

- Lafarge Africa Clears Debt, Posts ₦222bn Net Cash as Profit Jumps 173%

- ₦24trn in 8 Weeks: 30 Stocks Behind NGX’s Strong Start

- NGX Group Posts Modest Rise in Profit to N10.48bn

- NNPC Records ₦60.5trn Revenue, ₦5.7trn Profit in 2025

- 30 Banks Meet New Capital Threshold as Deadline Nears – CBN

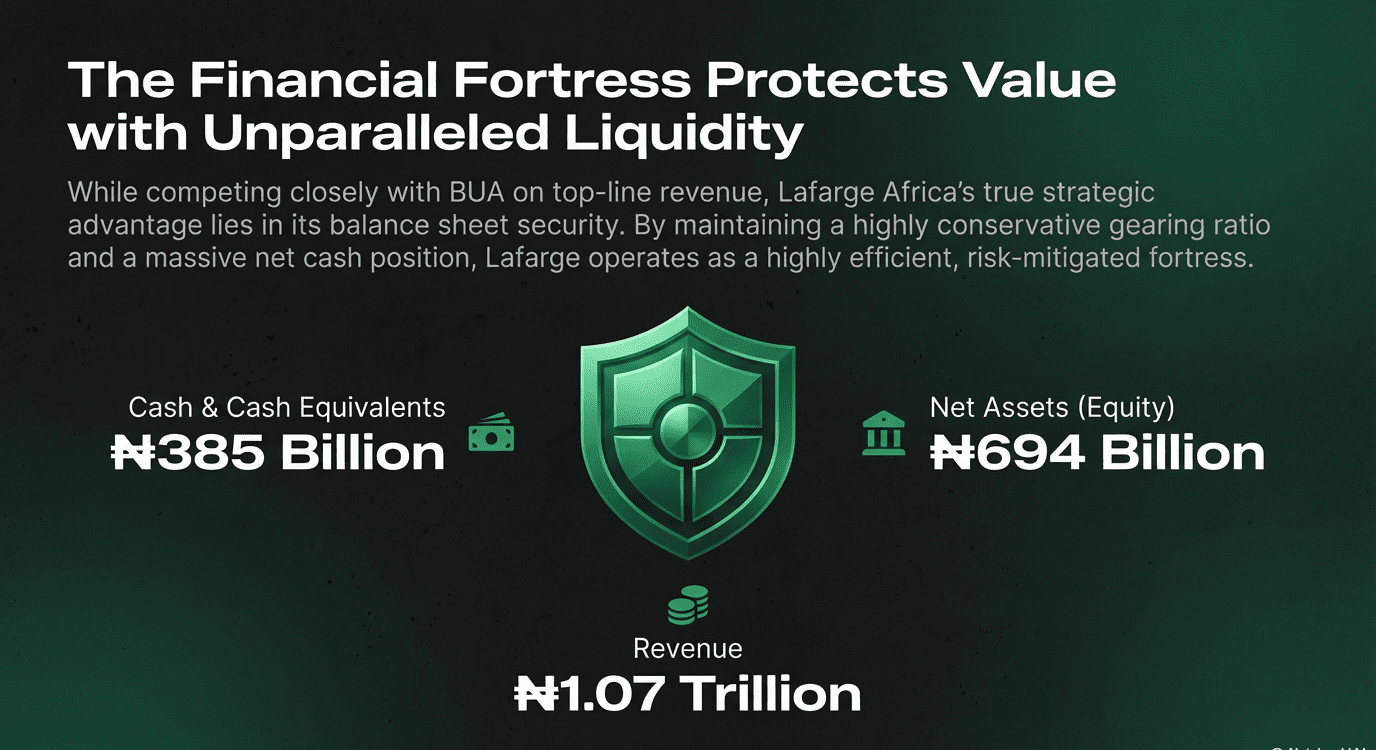

Lafarge Africa followed with a gross profit margin of 57.9 per cent, generating ₦617.4 billion in gross profit from revenue of ₦1.07 trillion.

BUA Cement reported the lowest margin at 51.23 per cent after recording gross profit of ₦604.2 billion on revenue of ₦1.18 trillion.

Despite having higher revenue than Lafarge, BUA Cement’s higher production costs reduced its margin, highlighting the stronger cost efficiency of its competitors.

Efforts to reduce cement prices have yet to materialise

In September 2023, when the Chairman of BUA Group, Abdul-Samad Rabiu, met with President Bola Tinubu, he declared that his company had initiated plans to reduce the price of a bag of cement in Nigeria from ₦5,500 at the time to between ₦3,000 and ₦3,500.

However, the much-anticipated reduction in the price of a bag of cement to ₦3,500, expected to take effect from October 1, 2023, has not materialised, with cement prices instead selling around ₦10,000 and above in recent years.

On Wednesday, March 13, 2024, the rising cement costs prompted the House of Representatives to move a motion to summon major cement manufacturers to discuss the persistent price increases and the hardship they have caused Nigerians.

The motion, titled ‘Arbitrary increase in cement price by cement manufacturers in Nigeria,’ was moved by Gaza Gbefwi from Nasarawa State and Ademorin Kuye from Lagos State.

Gbefwi argued that cement manufacturers have raised prices by up to 50 per cent despite most production inputs being sourced locally, questioning why¹ costs continue to rise.

“Demand for accommodation is rising, but supply has been inadequate. Supply will now be pressured by demand, and in that situation, rent will increase, which is already occurring,” said real estate expert and facility manager Stephen Jagun.

What drove Dangote’s superior margin

Dangote Cement’s superior margin was driven by its large production scale, strategic cost management and a revision in the useful life of its plants and buildings from 25 years to 40 years.

The accounting change reduced depreciation costs by ₦63 billion in 2025, helping to improve profitability.

The company’s scale also allows it to produce cement more efficiently.

While its revenue is nearly four times that of BUA Cement, its production costs are proportionally lower due to economies of scale and operational optimisation.

Lafarge saw the highest revenue growth

Dangote Cement recorded revenue of ₦4.31 trillion in 2025, representing a 20 per cent increase from ₦3.58 trillion in 2024.

Its net profit more than doubled to ₦1.02 trillion, while earnings per share rose to ₦59.86.

The board proposed a dividend of ₦45 per share, up from ₦30 in the previous year.

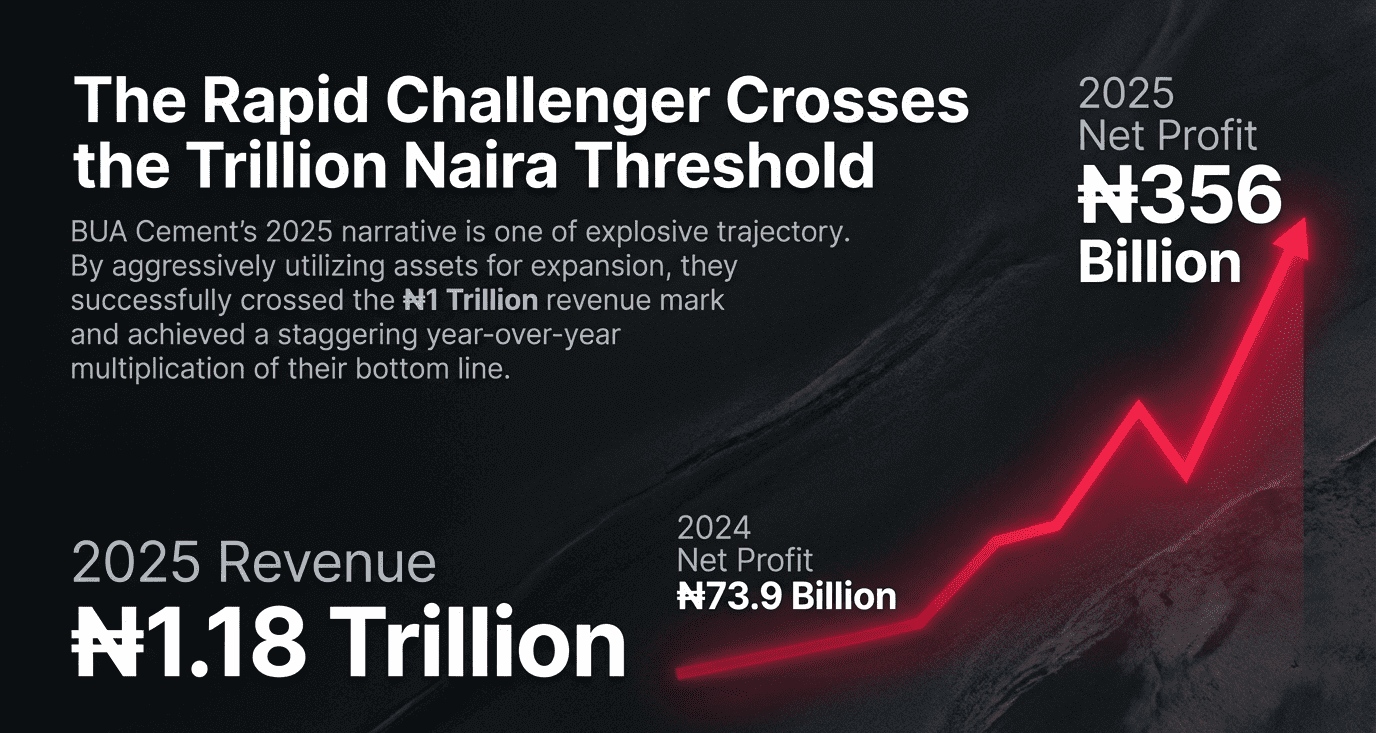

BUA Cement generated revenue of ₦1.18 trillion, up from ₦876.5 billion in 2024.

Its profit after tax surged to ₦356.04 billion from ₦73.91 billion, while earnings per share stood at ₦10.51.

The company recommended a dividend of ₦10 per share.

Lafarge Africa reported revenue of ₦1.07 trillion, representing a strong 53 per cent increase from ₦696.8 billion in the previous year.

Its profit for the year rose to ₦273.12 billion from ₦100.15 billion, while earnings per share reached ₦16.96.

Its board proposed a dividend of ₦6 per share.

Lafarge maintains the strongest financial position

Dangote Cement also remains the largest in terms of balance sheet strength.

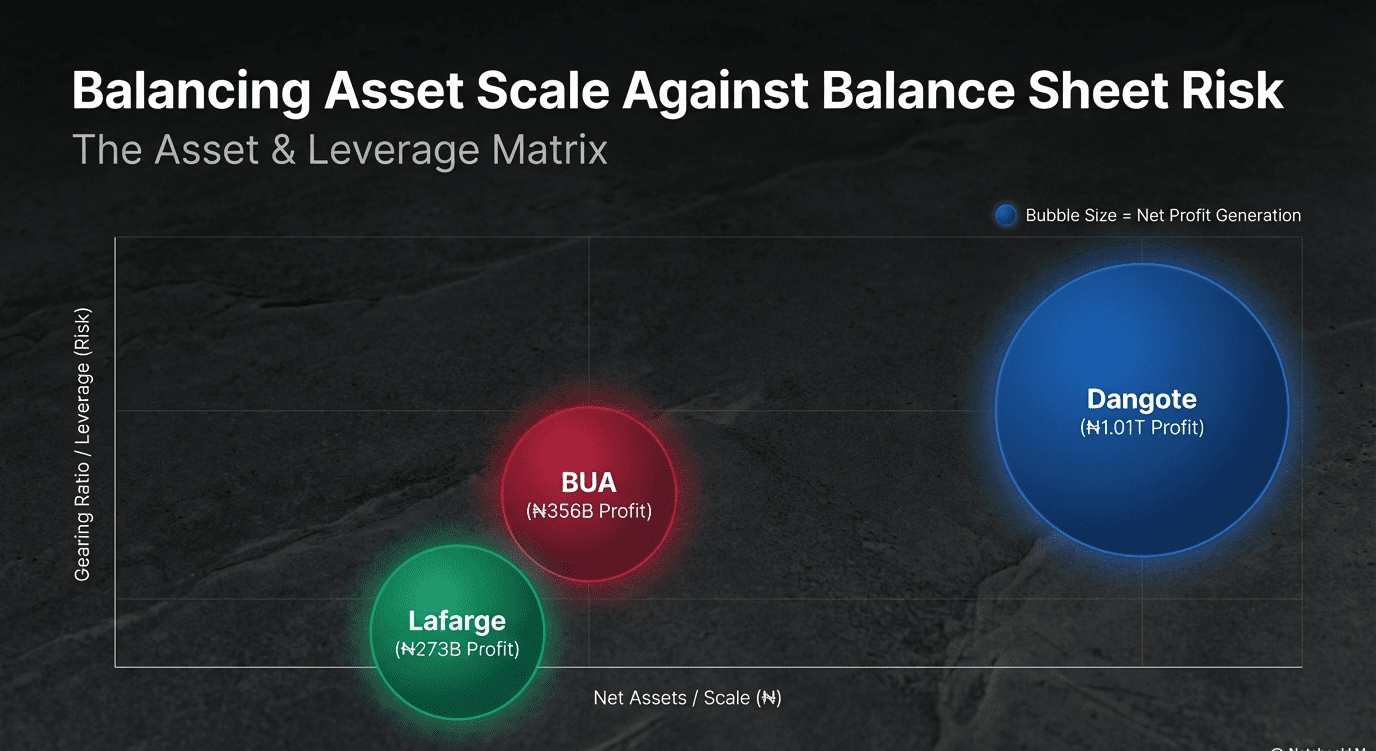

Total assets stood at ₦6.04 trillion as of December 31, 2025, while equity attributable to shareholders was ₦2.62 trillion.

The company improved its net debt-to-equity ratio to 0.26 from 0.95 in 2024, reflecting stronger balance sheet management.

Its market capitalisation closed the year at about ₦10.2 trillion.

BUA Cement reported total assets of ₦1.86 trillion and equity of ₦672.9 billion.

The company reduced its gearing ratio sharply to 37 per cent from 127 per cent a year earlier, supported by stronger liquidity and cash reserves.

Its market value stood at roughly ₦6.05 trillion.

Lafarge Africa recorded total assets of ₦1.21 trillion and equity of ₦694 billion.

The company maintained one of the strongest financial positions in the industry with a negative gearing ratio of –0.32, meaning it operates with more cash than debt.

During the year, China’s Huaxin Building Materials Group acquired an 83.81 per cent stake in the company from Holcim.

Dangote bears the highest operating risks

Dangote Cement also faces the most complex operating environment because of its wide footprint across Africa.

The company operates in several countries, including South Africa, Ethiopia, Tanzania, Zambia, Senegal and Cameroon, exposing it to multiple regulatory systems and volatile currencies.

Some markets, such as Sierra Leone, are classified as hyperinflationary, requiring special accounting adjustments.

Auditors flagged the need to assess potential impairment on about ₦252 billion invested in subsidiaries, some of which are currently loss-making and depend on financial support from the parent company.

The group also carries contingent liabilities of about ₦457.4 billion linked to pending legal claims and disputes.

BUA Cement’s main operational risk relates to litigation over mining licences in Okpella, Edo State, where a lawsuit is challenging the validity of four quarry licences. The company maintains that the claims are unlikely to succeed.

Lafarge Africa faces large contractual commitments through gas supply agreements valued at about ₦503.3 billion under take-or-pay arrangements.

However, its net cash position reduces financial risk compared with peers.

BUA, Lafrage lag in African expansion

Dangote Cement remains the most strategically positioned for future expansion across Africa.

The company already operates a broad manufacturing and grinding network across the continent, with operations in countries including Ethiopia, South Africa, Senegal, Cameroon, Tanzania, Zambia and Congo.

Its Pan-African operations contributed about ₦1.46 trillion, or roughly 34 per cent of total revenue in 2025.

Dangote Cement’s total production and bagging capacity stand at about 55 million tonnes per annum, with 25.75 million tonnes located outside Nigeria.

The company also manages property, plant and equipment worth about ₦3.9 trillion, including several projects under construction to expand capacity.

The group has built a vertically integrated system that includes limestone mining, coal production and power generation subsidiaries in several countries, helping secure raw materials and energy supply for its cement plants.

In contrast, BUA Cement’s manufacturing operations remain largely concentrated in Nigeria, with plants in Sokoto and Okpella.

Its international sales remain small, with only ₦14.8 billion in revenue generated outside Nigeria in 2025.

Lafarge Africa is also primarily focused on the Nigerian market after divesting its Ghana investment in 2021, although its acquisition by Huaxin Building Materials may influence future expansion plans.

Alex is a business journalist cum data enthusiast with the Pinnacle Daily. He can be reached via ealex@thepinnacleng.com, @ehime_alex on X