As the March 31 deadline for filing Pay As You Earn (PAYE) tax returns approaches, many Nigerians are trying to understand what exactly they need to do.

Online conversations show widespread confusion, especially among employees who assume that once their employer deducts tax, their responsibility ends.

However, filing a personal income tax return is a separate legal requirement, and missing the deadline can be costly.

According to the tax authorities, the penalties start at ₦100,000 for the first month and increase by ₦50,000 for every additional month of delay.

The process of filing, however, is not as complicated as it seems, as once an individual understands the steps and what is required, they can complete their filing entirely online.

Understanding What PAYE Really Covers

PAYE is a system where an employer deducts tax from an employee’s salary every month and sends it to the state’s tax authority. This applies to an employee’s salary, allowances, and any benefits received from his job.

However, PAYE only covers employment income. It does not account for other money an employee may earn outside his job.

It means that even if one’s employer has deducted tax throughout the year, an employee is still required to file an annual return to confirm that the correct tax was deducted and that all their income has been properly declared.

Mandatory Declaration of All Income

An employee’s tax is calculated based on their total income for the year, not just their salary. This means they need to include everything they earned in 2025, whether from their main job or other sources.

This includes income from side hustles, freelance work, rental earnings, dividends, interest, and any other form of income. As more Nigerians earn from multiple streams, especially through digital platforms, this step has become more important.

Once all your income is combined, allowable deductions can be applied to reduce the amount that will be taxed.

What Reduces Tax Bill

Not all income is taxed in full, as certain deductions are allowed under the law, and these can significantly reduce your tax burden.

These include pension contributions, housing fund payments, life insurance premiums, and rent-related reliefs within specified limits.

To benefit from these deductions, an individual needs to have proper records and be ready to declare them accurately when filing.

Where to File Tax Return

Personal income tax is handled at the state level, which means an individual must file their return with the tax authority in their state of residence or employment.

For employees, this is usually the state where they work, and for self-employed individuals, it is the state where they live. Even if an individual earns income from different places, their filing is tied to their primary location.

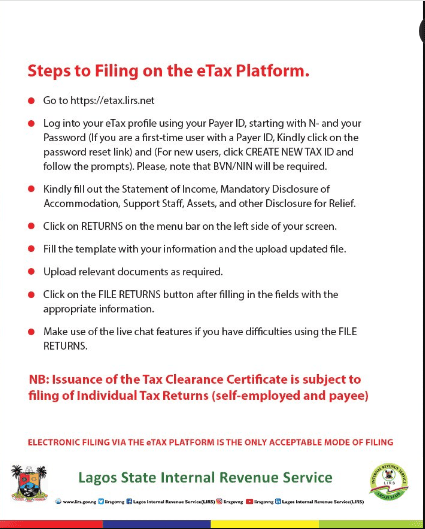

The Entire Process is Now Online

Tax filing in Nigeria is now fully digital, removing the need to visit physical offices. To begin, an individual needs a Taxpayer Identification Number.

If an individual does not already have one, he or she can register on their state’s tax portal using their Bank Verification Number (BVN) and date of birth.

READ ALSO:

- LIRS Urges Taxpayers to File Returns Ahead of March Deadline

- CPPE Calls for Targeted Approach to Enforcing New Tax Laws

- CBN Adds $3.5bn in Locally Sourced Gold to Reserves

- Foreign Firms Pay More as Nigeria’s CIT Hits ₦2.96trn in Q3

- CBN Ends Dollar Payouts for Diaspora Remittances

After registration, an individual can log in to the platform, locate the returns section, and begin the filing process.

Filing Your Tax Return

When you start your return, you will be required to provide details about your income and financial activities for the year. You will select the relevant year, which is 2025 for filings done in 2026.

You will then enter your gross salary, which is your total earnings before deductions, along with any additional income you received.

The form also provides sections to include pension contributions, investment income, rent paid, and rental income if applicable.

If you earn from multiple sources, all of them must be declared. Accuracy is important because tax authorities can verify your information through your bank, employer, and financial records.

Documents Needed

Supporting documents are required to validate the information you provide. These include bank statements, rent receipts or tenancy agreements, and proof of pension contributions or insurance payments.

These documents help confirm your claims and ensure that your tax is calculated correctly.

What Happens after Submission

Once you submit your return, the system automatically calculates your total tax liability. Any tax already paid through PAYE is deducted from this amount.

If there is a balance left to pay, you can complete the payment online or through designated banks. If your previous payments cover your liability, your records will reflect that.

If You Earn from Multiple Sources

According to the Presidential Fiscal Policy and Tax Reforms Committee, in one of their lecture series, for individuals with multiple income streams, filing requires extra attention.

All income must be combined before calculating tax to ensure that the full amount is assessed correctly.

Some types of income, such as dividends or interest, may already have withholding tax deducted at source.

In some cases, this deduction is treated as the final tax, meaning no additional payment is required. However, the income must still be declared.

Non-cash benefits provided by employers, such as housing or official vehicles, are also considered part of your income and must be included.

Freelancers and remote workers are taxed based on where they live, even if they work for foreign employers, as long as the work is performed within Nigeria.

Tax Rules to Use for Filing

Although new tax rules came into effect in 2026, they do not apply to this filing cycle. When filing in 2026, you are reporting income earned in 2025, so the previous tax rates must be used.

The updated rules will only apply when filing returns for 2026 income in 2027.

Bottom Line

Filing a PAYE return is not optional; even if your employer has deducted tax throughout the year, you are still required to submit an annual return declaring all your income.

The process is now easier because it is fully online, but it still requires careful attention and proper documentation.

Starting early and understanding the steps involved can help you avoid stress and penalties while ensuring that your tax records are accurate.

Alex is a business journalist cum data enthusiast with the Pinnacle Daily. He can be reached via ealex@thepinnacleng.com, @ehime_alex on X