For more than a decade, Nigeria’s small and medium-scale enterprises (SMEs), the country’s largest employers and backbone of the real economy, have remained largely excluded from formal bank financing, despite repeated policy pledges to support them.

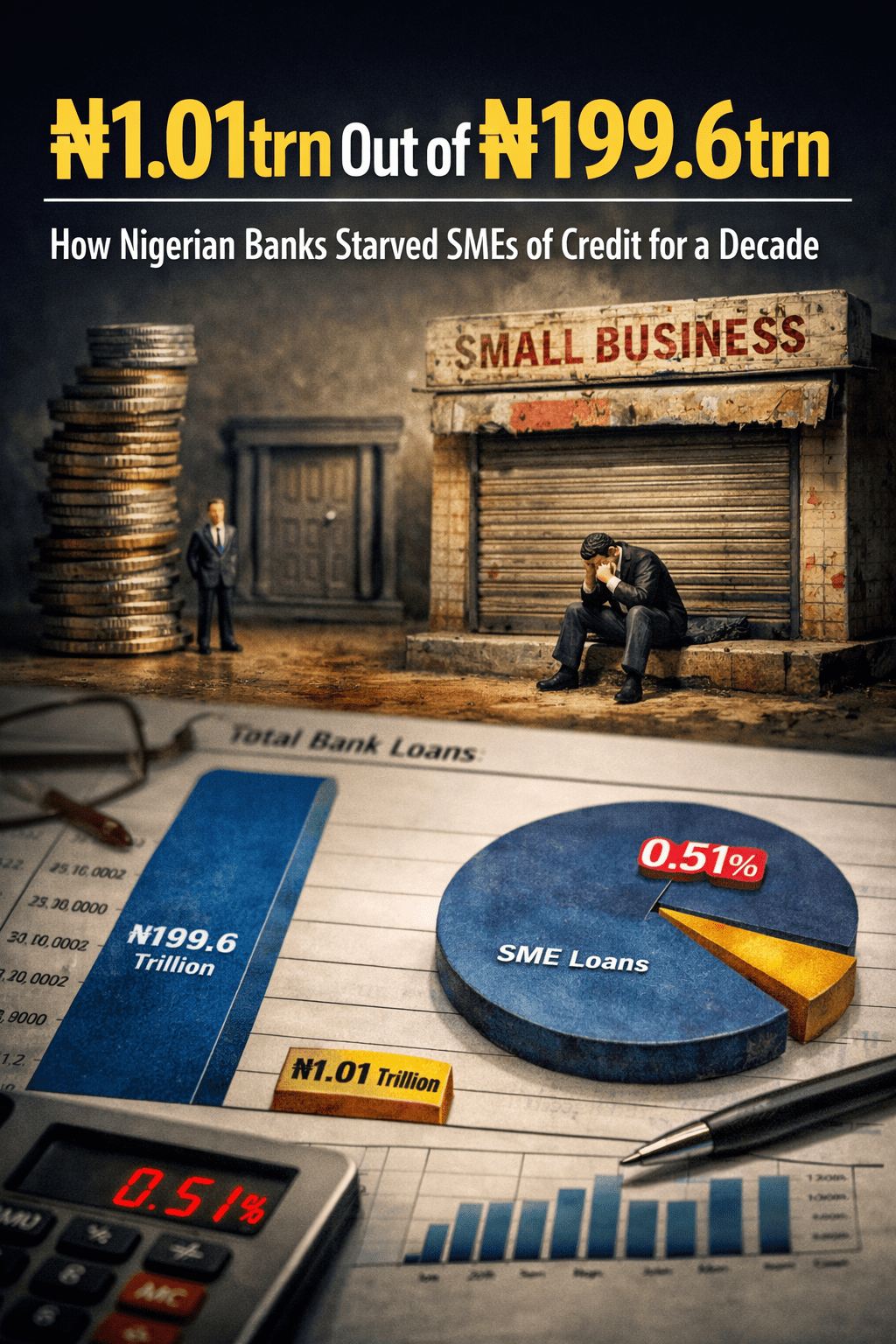

An analysis of the Central Bank of Nigeria (CBN) Statistical Bulletin covering 2014 to 2023 reveals a troubling reality: SMEs received just 0.51 per cent of total bank credit to the private sector over the period, underscoring one of the most persistent structural weaknesses in Nigeria’s financial system.

Out of ₦199.63 trillion in total loans extended to the private sector within the 10 years, SMEs accessed only ₦1.01 trillion, leaving them severely underfunded in an economy where they account for over 80 per cent of jobs.

The data show that SME lending has not only been low, but it has also been wildly inconsistent.

In 2014, banks disbursed ₦116.07 billion to SMEs out of a total ₦1.32 trillion, representing 0.88 per cent of total private-sector credit. But this modest share collapsed dramatically in 2015, when SME credit plunged to just ₦2.95 billion, or 0.02 per cent.

Between 2016 and 2017, lending stagnated at ₦10.75 billion annually, accounting for 0.07 per cent of total credit. A mild recovery followed in 2018, when SMEs received ₦44.82 billion (0.29 per cent), before rising further to ₦123.93 billion (0.71 per cent) in 2019.

The momentum did not last.

In 2020, SME credit fell again to ₦62.51 billion (0.32 per cent), inching up slightly to ₦83.74 billion (0.38 per cent) in 2021 and ₦93.45 billion (0.36 per cent) in 2022.

Although 2023 recorded a notable improvement—₦465.37 billion out of ₦3.93 trillion, or 1.18 per cent, the highest share in the decade—analysts warn that the figure remains marginal and insufficient to drive meaningful SME-led growth.

A ₦48 Trillion Financing Gap

The weak flow of bank credit to SMEs stands in stark contrast to Nigeria’s massive ₦48 trillion MSME financing gap, according to a PwC 2024 report.

Despite the presence of intervention agencies such as the Bank of Industry (BoI), the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN), and other development finance institutions (DFIs), the funding shortfall persists.

Commercial lending rates frequently exceed 30 per cent, while loan tenors rarely extend beyond three years, making it nearly impossible for SMEs to invest in machinery, scale production, or adopt new technologies.

READ ALSO:

-

SMEDAN Moves to Launch Microfinance Bank, Seeks CBN Licence

-

SEC, SMEDAN Sign MoU to Improve Funding for SMEs

-

FG Launches SME Growth Dialogue

-

CBN Licenses Apices Finance to Boost SME’s Lending

In an exclusive interview with Pinnacle Daily, investment banker Sidiku Olayinka Oscars said the marginalisation of SMEs is not accidental but rooted in deep structural issues within Nigeria’s banking ecosystem.

“CBN data clearly show that SMEs received just about 0.5 per cent of total bank credit over a decade,” Oscars said. “From an investment banking perspective, banks have continued to sideline SMEs largely because of higher perceived credit risk.”

According to him, most SMEs lack structured accounting systems, internal policies, and auditable financial records, making it difficult for banks to assess their true financial health.

“Without audited financial statements and clean credit histories, assessing SME loan applications becomes almost impossible for commercial banks,” he explained.

Another major obstacle, according to him, is collateral.

“Most SMEs do not possess traceable, properly valued fixed assets such as landed properties or buildings that banks require to mitigate default risk,” Oscar added.

Policy Constraints and a Harsh Monetary Environment

Beyond firm-level weaknesses, macroeconomic and regulatory factors have also constrained SME lending.

Nigeria’s tight monetary environment, characterised by interest rates hovering between 35 and 40 per cent, depending on the bank, has made SME loans prohibitively expensive. In addition, liquidity policies such as the 50 per cent Cash Reserve Ratio (CRR) have incentivised banks to prioritise large, low-risk corporate clients over smaller, more vulnerable businesses.

As a result, Nigeria’s industrial strategy has increasingly favoured large firms, limiting broad-based industrialisation and job-rich growth.

While institutions such as the BoI and the Development Bank of Nigeria (DBN) have made modest gains, their scale remains limited.

According to the BoI 2024 Annual Report, only 15.3 per cent (₦78.2 billion) of the ₦510.9 billion disbursed in the year went to micro, small and medium enterprises. Meanwhile, SMEDAN data show that about 79 per cent of MSMEs still rely on personal savings to finance their operations, a clear sign of exclusion from formal credit markets.

Can Reforms Unlock Sustainable SME Credit?

With lending rates above 30 per cent and short loan tenors choking SME growth, analysts say structural reforms, not temporary interventions, are required.

Oscars points to recent institutional reforms under the Tinubu administration aimed at bypassing commercial lending bottlenecks through government-backed de-risking mechanisms.

One such initiative is the National Credit Guarantee Company (NCGC), which provides up to 60 per cent credit guarantee coverage on loans extended to MSMEs through commercial banks, microfinance institutions, and fintechs.

READ ALSO:

- Calls for Decentralised Power System Intensify as Grid Failure Persists

- Oil, Gas Resources Remain Vital to Africa’s Development – NUPRC CEO

- Why Fixing Nigeria’s Broken Supply Chains Could Unlock Billions, Redefine the Economy

“Risk-sharing is key,” Oscar said. “When banks know that part of the loan is guaranteed, their appetite for SME lending increases.”

In addition, the ₦200 billion MSME Fund offers loans of up to ₦5 million at 9 per cent interest, with tenors of up to three years, targeting manufacturers and small businesses.

SMEDAN is also brokering ₦12 billion in funding for 2026, with interest rates between 9 and 9.5 per cent, aimed at business expansion and equipment financing.

The Bigger Question

While these reforms signal progress, analysts caution that without widespread adoption, stronger credit infrastructure, and improved SME governance standards, Nigeria risks repeating a familiar cycle where SMEs remain celebrated in policy speeches but neglected in credit allocation.

For an economy seeking inclusive growth, the question remains: Can Nigeria truly industrialise while starving its biggest job creators of capital?

Until that question is answered decisively, the data suggest that SMEs will continue to operate not as partners in growth but as outsiders in Nigeria’s banking system.

Esther Ososanya is an investigative journalist with Pinnacle Daily, reporting across health, business, environment, metro, Fct and crime. Known for her bold, empathetic storytelling, she uncovers hidden truths, challenges broken systems, and gives voice to overlooked Nigerians. Her work drives national conversations and demands accountability one powerful story at a time.