When Jim Ovia, founder and immediate past chairman of Zenith Bank, said recently that real estate pays more than banking, many saw it as the retirement move of one of Nigeria’s most successful entrepreneurs. But his decision points to a broader shift in Nigeria’s economy, where inflation, exchange-rate volatility and high borrowing costs are increasingly making property more attractive than productive investment.

After building one of Nigeria’s biggest banks, Ovia is expanding into luxury real estate through Quantum Luxury Properties. The company is said to be developing Metropolitan Towers, a 26-floor residential building where apartments will sell for $1.85 million each, alongside Quantum Luxury Towers, where prices start from $2.8 million.

Coming from a banker whose career was built on financial intermediation, the move raises an important question: has Nigeria reached a point where owning property offers better long-term returns than financing businesses?

Evidence from bank balance sheets, macroeconomic data and investment trends suggests Nigeria’s investment incentives are increasingly favouring tangible assets that preserve wealth over productive enterprises, Pinnacle Daily analysis shows.

Balance Sheets Reflect the Shift

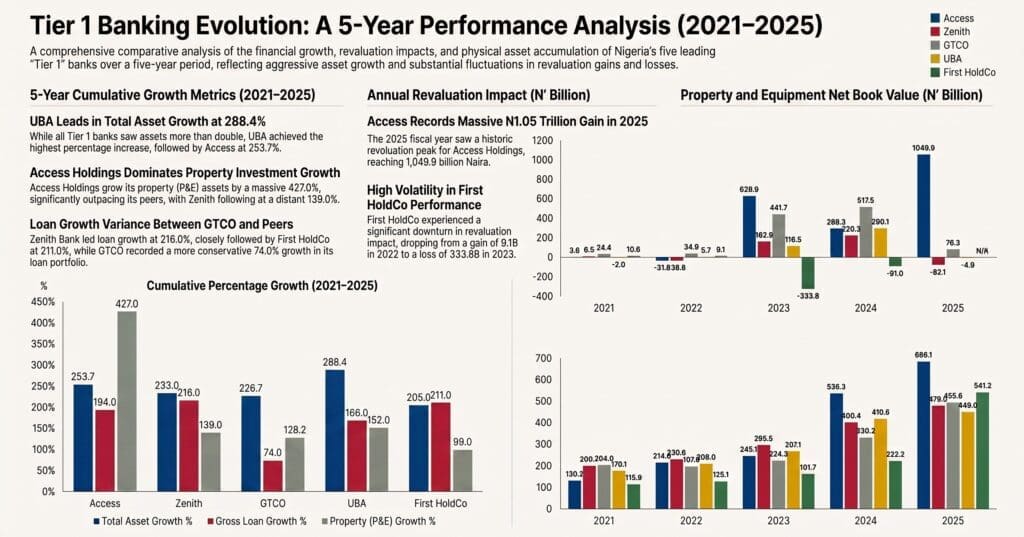

A review of audited financial statements of Nigeria’s largest banks between 2021 and 2025 reveals a consistent pattern. Property assets have expanded rapidly even as customer lending has become a smaller share of growing balance sheets.

Access Holdings provides the clearest example as its property and equipment portfolio grew from ₦130.2 billion in 2021 to ₦686.1 billion in 2025, representing a 427 per cent increase. During the same period, total assets rose by 253.7 per cent while loan growth, though strong at 194 per cent, lagged behind both.

GTCO followed a similar path as property assets expanded by 128.2 per cent compared with loan growth of about 74 per cent, while its loan-to-asset ratio fell sharply from 33.2 per cent in 2021 to 17.6 per cent in 2025.

UBA’s total assets increased by 288.4 per cent against loan growth of 167.6 per cent, reducing the share of lending within its balance sheet. Zenith Bank also recorded substantial growth in property assets as land, buildings and branch infrastructure appreciated.

While the figures do not show banks abandoning lending, they instead show property assets becoming increasingly valuable while loans account for a smaller proportion of expanding balance sheets.

Part of the increase reflects branch expansion across Africa, while exchange-rate translation and hyperinflation accounting also lifted the naira value of foreign properties. Nevertheless, the trend is clear: physical assets have become increasingly important stores of value.

First HoldCo offers another example, as through Rainbow Town Development Limited, the group held property worth ₦531.2 billion before classifying it as held for sale in 2024. Although it remains the only Tier 1 bank with a significant property development subsidiary, the asset illustrates the growing importance of real estate within parts of Nigeria’s financial system.

The balance sheets also show that total assets have generally grown faster than loan books, suggesting banks are increasingly strengthening positions in physical infrastructure, sovereign securities and other lower-risk assets capable of preserving value during periods of economic uncertainty.

That shift coincided with one of Nigeria’s most volatile economic periods.

Headline inflation climbed from 16.47 per cent in January 2021 to a peak of 34.80 per cent in December 2024 before moderating to 15.93 per cent by May 2026. During roughly the same period, the Monetary Policy Rate (MPR) rose from 11.5 per cent to 27.5 per cent before easing slightly to 26.5 per cent.

The naira also weakened dramatically, moving from around ₦381-₦393 to the dollar in early 2021 to ₦1,660 in December 2024 before recovering to about ₦1,379 by July 2026.

Together, these developments reshaped investment incentives, as inflation eroded the value of financial assets, high interest rates made borrowing more expensive and lending riskier, while currency depreciation increased the replacement value of physical assets. Property increasingly became a store of wealth capable of preserving value while generating rental income and capital appreciation.

Ovia’s remark therefore reflects more than a personal investment decision, mirroring broader economic conditions that have steadily changed where Nigerian capital finds its highest returns.

READ ALSO:

- Banks Raise ₦4.65trn as CBN Wraps Up Recapitalisation Exercise

- Foreign Tax Reliance Exposes Nigeria’s Economic Weakness

- Zenith Bank Founder Jim Ovia Bows Out as Chairman

- IMF Sees Stable Growth for Nigeria, Flags Four Key Risks

- Zenith Bank Confirms Expansion Plans to East Africa

Why Property Keeps Attracting Capital

The attraction of real estate extends well beyond bank balance sheets.

According to official data, Nigeria’s housing deficit is estimated at 14.99 million units, while its population of about 227 million requires more than 550,000 new homes every year. Demand continues to outstrip supply, creating sustained opportunities for investors.

Similarly, data from Statista shows that Nigeria’s real estate market will be worth $2.42 trillion in 2026, with residential property accounting for $2.05 trillion. By 2031, the market is expected to grow to $2.83 trillion, supported by continued demand for housing and luxury developments.

Former First Bank Chairperson, Ibukun Awosika, believes those returns explain why international investors continue to commit capital to Nigeria despite concerns over country risk.

“For those of you who are abroad and want to invest in Nigeria, if you know what you’re doing and you’re organised about it, the return on investment you can get in Nigeria is something you can never get in the economies where you live.”

She argued that Nigeria’s challenge is often one of perception rather than opportunity.

“All the money that funds are giving out comes from international investors around the world. Why do you think they are putting their money in Africa? It is because of the high returns.”

Awosika, however, cautioned that successful property investment depends on understanding where demand exists rather than simply buying luxury assets.

“We need to align our investments with market realities,” she said, arguing that the strongest housing demand lies in affordable homes rather than high-end developments concentrated in Ikoyi, Victoria Island and Lekki.

Her comments reinforce a central theme that investors increasingly see property as a reliable means of preserving wealth in an economy marked by inflation and currency volatility.

Cost of Capital Is Reshaping the Economy

Real estate entrepreneur Femi Rogers argues that Nigeria’s housing market also exposes a deeper weakness in the country’s financial system: the limited availability of affordable long-term finance.

“In Nigeria, developers often rely entirely on their own capital. It is essentially a cash-on-cash model. You build with all the money you have,” he said.

He contrasted that with the United States, where developers typically contribute about 20 per cent of a project’s cost while banks finance the remaining 80 per cent through construction loans.

“If I were developing property in Nigeria, I would need ₦1 billion in cash to build one house. In the United States, the same ₦1 billion in equity allows me to build five houses because I am leveraging bank financing.”

The comparison highlights an irony that although property has become one of Nigeria’s preferred investment destinations, access to financing for housing development remains shallow. Developers rely heavily on personal capital instead of bank credit, limiting the pace at which new housing can be delivered despite strong demand.

The same forces driving investors towards property are also making credit more expensive for productive businesses.

As interest rates climbed alongside the MPR, banks faced higher lending risks while businesses struggled with rising borrowing costs. The result has been a more cautious approach to lending, with banks strengthening positions in lower-risk assets while loan books account for a smaller share of their expanding balance sheets.

That does not mean lending has become unprofitable, as interest income has continued to grow strongly across the banking industry. Rather, it suggests that preserving capital has become just as important as deploying it.

For manufacturers, however, the implications are profound.

Despite repeated government commitments to industrialisation, manufacturers continue to argue that affordable long-term financing remains one of the sector’s biggest constraints.

Pinnacle Daily reports that the Manufacturers Association of Nigeria (MAN) had called for a Manufacturing Refinancing and Rediscounting Facility that would enable banks to refinance manufacturing loans at single-digit interest rates for up to seven years.

The association has also sought a ₦1 trillion stabilisation fund, increased capitalisation of the Bank of Industry (BOI), greater transparency around lending flows and lower benchmark interest rates.

Those requests reflect a wider concern, as when borrowing costs remain prohibitively high, businesses postpone investment, expansion slows, and industrial growth becomes harder to achieve.

Recently, the Centre for the Promotion of Private Enterprise (CPPE) shared the same concern, noting that Nigeria’s manufacturing sector has remained largely stagnant, contributing only about nine to 10 per cent of Gross Domestic Product (GDP) despite 26 years of democratic rule.

“Many successful manufacturers have thrived not because conditions were favourable, but despite formidable policy, regulatory and infrastructural obstacles,” CPPE’s Chief Executive Officer, Dr Muda Yusuf, said.

“No manufacturing economy can achieve global competitiveness when power is unreliable, logistics are inefficient, and capital is prohibitively expensive.”

His comments capture the broader consequence of changing investment incentives. If property consistently delivers stronger and more predictable returns than productive enterprise, capital will naturally gravitate towards assets that preserve wealth instead of businesses that create jobs and expand output.

What Ovia’s Remark Really Means

Jim Ovia’s statement is ultimately much more than real estate, as it reflects an economy where inflation, exchange-rate volatility and elevated borrowing costs have steadily changed the way investors think about risk and returns.

Property has become more than a physical asset; it has evolved into a preferred store of wealth in an uncertain macroeconomic environment.

The evidence does not suggest Nigerian banks are transforming into property companies; rather, it shows financial institutions adapting to economic realities by placing greater value on assets that protect their balance sheets while lending more cautiously.

At the same time, local and international investors continue to see Nigerian real estate as one of the country’s most attractive asset classes because of its potential for capital appreciation and recurring income.

This presents a dilemma for policymakers. While property investment is essential to reducing Nigeria’s housing deficit, long-term economic growth depends on ensuring that enough capital also flows into manufacturing, agriculture and other productive sectors capable of creating jobs, raising productivity and expanding exports.

Ovia may have been talking about his next investment, but his remark has exposed a much bigger question about Nigeria’s economy.

That is, if one of Nigeria’s most accomplished bankers believes real estate pays more than banking, what does that say about the incentives shaping capital allocation?

Until those incentives shift, Nigeria may continue to witness more capital flowing into buildings than businesses—a trend that could enrich investors but leave the country’s industrial ambitions struggling for finance.

Alex is a business journalist cum data enthusiast with the Pinnacle Daily. He can be reached via ealex@thepinnacleng.com, @ehime_alex on X