After benefiting from one-off gains triggered by the naira’s sharp devaluation, banks are now returning to a more sustainable growth model built on stronger lending, digital banking and fee-based businesses, Pinnacle Daily analysis shows.

An analysis of the audited financial statements of Access Holdings, Zenith Bank, United Bank for Africa (UBA), GTCO and First HoldCo between 2021 and 2025 shows that interest income became banks’ most powerful and consistent revenue driver, while non-interest income delivered exceptional but temporary gains during the height of the foreign exchange crisis.

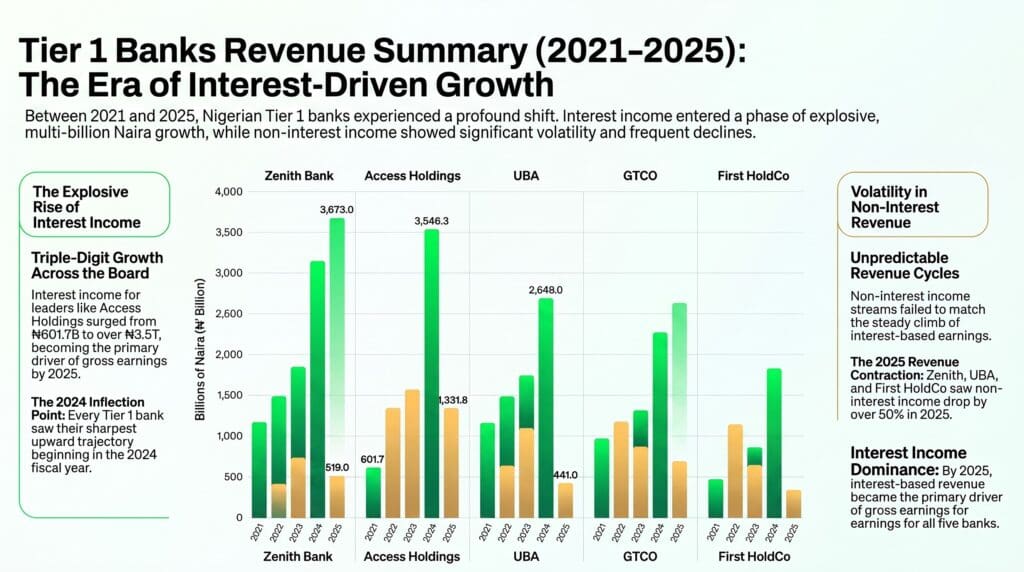

The figures reveal that interest income expanded far more rapidly than non-interest income across all five banks during the review period, underscoring a strategic shift back to traditional banking activities after the foreign exchange windfall began to fade.

Zenith Posted Highest Income Growth

Zenith Bank led the industry in interest income growth in absolute terms. Its interest income climbed from ₦427.6 billion in 2021 to ₦3.67 trillion in 2025, an increase of more than eightfold.

Access Holdings followed closely, growing interest income from ₦601.7 billion to ₦3.55 trillion over the same period as it expanded its balance sheet and loan portfolio across multiple markets.

UBA also recorded remarkable growth, with interest income rising from ₦474.3 billion in 2021 to ₦2.65 trillion in 2025.

Much of that expansion came between 2023 and 2024, when the bank more than doubled its interest income, supported by stronger lending activities and improved net interest margins across its operations in 20 African countries.

GTCO’s interest income followed the same trajectory, increasing from ₦266.9 billion in 2021 to ₦1.65 trillion in 2025, representing growth of more than 500 per cent.

First HoldCo also experienced a similar trend. Although it does not always disclose a single consolidated interest income figure in its primary financial summaries, its gross earnings grew from ₦757.3 billion in 2021 to ₦3.44 trillion in 2025, with interest-bearing assets accounting for the largest share of that growth.

The surge in interest income reflected the operating environment during the period.

It shows that rising interest rates allowed banks to reprice loans, while higher yields on government securities and other investment assets boosted returns.

Non-interest Income Surged

As banks expanded their loan books and invested more heavily in high-yield securities, interest income became the dominant source of earnings by 2024 and 2025.

Non-interest income also grew significantly but followed a very different pattern.

Unlike interest income, which recorded steady expansion throughout the period, non-interest income was driven largely by extraordinary gains arising from the naira’s devaluation.

READ ALSO:

- Beyond Lending: Nigerian Banks Bet Big on Non-Banking Businesses

- Risks, Opportunities: US-Iran War Poses for Nigeria

- Higher Taxes, Non-Interest Losses Drag GTCO’s 2025 Earnings Down

- CBN Moves to Raise ATM Card Fee, Cut Other Bank Charges

- Five Key Issues That Shaped Zenith Bank Performance in 2025

These gains came mainly from foreign exchange revaluation, trading income, fees and commissions, and other operating income.

For most banks, 2024 represented the peak of this windfall.

Zenith Bank recorded the highest non-interest income among its peers, reaching ₦1.25 trillion in 2024 before falling sharply to ₦519 billion in 2025 as foreign exchange gains normalised.

GTCO’s non-interest income rose from ₦180.9 billion in 2021 to a peak of ₦808.6 billion in 2024 before moderating to ₦497.1 billion in 2025.

The strongest contributor during the peak years was foreign exchange revaluation, although fee and commission income continued to grow steadily throughout the review period.

Access Holdings recorded one of the most balanced performances. While benefiting from foreign exchange gains, the group also strengthened recurring fee income through its expanding digital banking channels.

By 2025, fee and commission income had grown to ₦754.6 billion, supported largely by channels and e-business income, while total non-interest income stood at an estimated ₦1.33 trillion.

UBA relied less on one-off gains than many of its peers. Its extensive presence across 20 African countries continued to generate stable transaction-based income through fees and commissions.

Net fee and commission income reached ₦532.9 billion in 2025, although trading and foreign exchange income weakened following fair value losses on derivatives.

Overall non-interest income declined to ₦441 billion after reaching much higher levels during the foreign exchange boom.

First HoldCo also experienced significant swings in non-interest income. Revenue from fees, foreign exchange transactions, trading gains and dividend income climbed to an estimated ₦1.06 trillion in 2024 before easing to about ₦786.4 billion in 2025 as the exceptional foreign exchange gains moderated.

Across the five banks, one component of non-interest income, that is, fee and commission income, remained remarkably resilient

As more customers embraced electronic banking, digital payments and card transactions, fee income continued to rise steadily.

Access Holdings reported ₦215.3 billion from channels and other e-business activities in 2025, while GTCO, Zenith Bank and UBA also strengthened earnings from account maintenance charges, card services and electronic transactions.

Dividend income from subsidiaries and investments provided an additional source of stable earnings.

A Shift Towards Sustainable Earnings

The pattern emerging from the five-year review suggests that Nigerian banks are moving beyond earnings driven by temporary market conditions and returning to growth supported by their core businesses.

According to Oluwayemisi Sunmola, banking analyst at Vetiva Capital Management, 2025 marked a transition from the volatility experienced in the previous two years.

“We are seeing the banks move away from the FX-related volatility and the higher MPR rates we saw during the 2023 and 2024 period,” he said on an ARISE TV programme.

“We saw that 2025 was more of a stabilisation year for the banks, where many of them recorded moderation in their FX income due to the relative stability of the naira. At the same time, banks generally recorded stronger core income.”

Sunmola expects the trend to continue in 2026 as earnings become more sustainable.

“We expect that, given the moderation in FX volatility, 2026 will be a year of building on the gains recorded in 2025. As a result, we expect more sustainable earnings generation, as well as stronger fundamentals,” he said.

He explained that while higher interest rates and asset repricing were the biggest drivers of bank earnings in recent years, the next phase of growth would come from stronger loan expansion as banks deploy fresh capital raised through recapitalisation.

“In 2025, banks recorded a significant portion of their earnings from asset repricing following the increases in the MPR. For 2026, we expect the growth story to shift more toward loan expansion. Given that banks now have stronger capital buffers and are better positioned to absorb shocks, we see this as a major driver of earnings growth.”

Sunmola also expects lower funding costs to support profitability, particularly for banks with strong current and savings account franchises such as GTCO and Zenith Bank.

“We expect the cost of funds to trend lower as interest rates decline. Given the expansion in their loan books, we expect that to drive up interest income.

“Consequently, we expect net interest margins to remain stable or record slight expansion in 2026,” he said.

Beyond lending, he believes digital banking will remain an important contributor to non-interest income as electronic transactions continue to rise.

“We expect digital expansion to continue as online transactions increase,” he said. “This should encourage greater adoption of digital payment channels, which will, in turn, support growth in banks’ fee income.”

Pinnacle Daily had earlier analysed how Nigerian banks are increasingly generating income from businesses that have little to do with traditional banking, including from pensions and asset management to payment services, insurance brokerage and digital lending.

Alex is a business journalist cum data enthusiast with the Pinnacle Daily. He can be reached via ealex@thepinnacleng.com, @ehime_alex on X