The Central Bank of Nigeria’s (CBN) revocation of operating licenses for 46 microfinance banks (MFBs), effective July 1, 2026, is the latest chapter in a decade-long effort to clean up a sub-sector that has long struggled to reconcile its social mandate, extending credit to Nigeria’s unbanked and underbanked, with the discipline of prudential banking.

Acting under Sections 12 and 13 of the Banks and Other Financial Institutions Act (BOFIA) 2020, CBN Governor Olayemi Cardoso approved the action after the affected institutions failed on one or more of five fronts: insufficient assets to cover liabilities, unauthorized closure of operations, prolonged inactivity and cessation of financial intermediation, failure to commence business within 12 months of licensing, and inability to maintain minimum capital unimpaired by losses.

The announcement, which was made in a statement signed by the CBN’s Acting Director of Corporate Communications, Hakama Sidi-Ali, and the Nigeria Deposit Insurance Corporation (NDIC), has since been appointed liquidator, pursuant to Section 12(2) of BOFIA 2020 and Sections 55(1&2) of the NDIC Act 2023.

A familiar, recurring story—but not identical to the last one

This is not an isolated event. The CBN revoked 132 MFB licenses (alongside primary mortgage banks and finance companies) in May 2023 under then-Governor Godwin Emefiele and 42 MFBs in November 2020. The recurrence suggests the sub-sector’s fragility is structural rather than episodic—a mix of undercapitalization, weak corporate governance, and, in some cases, outright abandonment of operations by promoters who never truly committed to the business.

It is worth being precise about the timing, because the two big regulatory clocks running in Nigerian banking this year are not the same clock. The CBN’s headline recapitalization deadline—March 31, 2026, requiring deposit money banks to raise fresh capital of up to ₦500 billion for international license holders—applied to commercial banks, not microfinance banks; only 30 of them had met the new threshold by early March.

Microfinance banks operate under their own, much smaller capital regime: ₦50 million for Tier 2 (rural) MFBs, ₦200 million for Tier 1 (urban) MFBs, ₦1 billion for state-licensed MFBs, and ₦5 billion for national MFBs.

The 46 revocations sit alongside, not inside, the DMB recapitalization drive—but the same underlying supervisory logic applies: institutions unable to meet even these modest thresholds, or to demonstrate genuine financial intermediation, are being weeded out.

Where the failures are concentrated

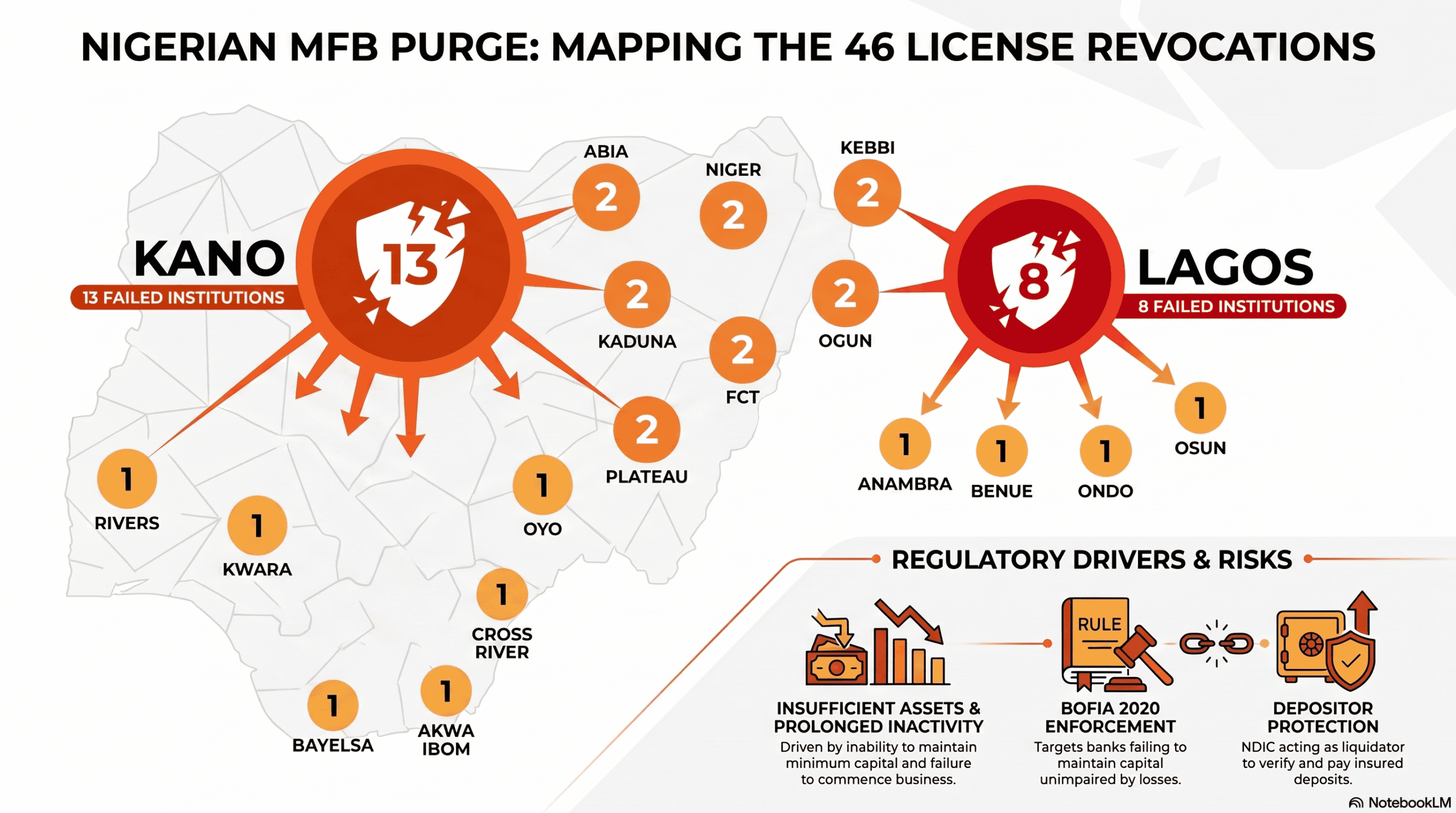

A state-by-state breakdown of the 46 affected banks, drawn from the CBN and NDIC’s published list, shows a lopsided geography that should interest anyone tracking regional financial inclusion trends:

| State | MFBs affected | Share of total |

| Kano | 13 | 28.3% |

| Lagos | 8 | 17.4% |

| Abia, Niger, Kebbi, Ogun, Plateau, Kaduna, FCT (Abuja) | 2 each — 14 total | 30.4% |

| Rivers, Kwara, Bayelsa, Delta, Oyo, Cross River, Akwa Ibom, Anambra, Benue, Ondo, Osun | 1 each — 11 total | 23.9% |

Two states dominate. Kano alone accounts for 13 of the 46 licenses revoked—just over 28 percent of the total—while Lagos contributes eight, or roughly 17 percent. Together, these two commercial hubs account for nearly half (45.7 percent) of all the failures, despite representing a fraction of Nigeria’s 36 states plus the FCT. Seven other states—Abia, Niger, Kebbi, Ogun, Plateau, Kaduna, and the FCT—recorded exactly two failures each, pointing to a broader, if less concentrated, national problem rather than one confined to a single region.

READ ALSO:

- CBN Revokes Licences of 46 Microfinance Banks

- SMEDAN Moves to Launch Microfinance Bank, Seeks CBN Licence

- How Nigerian Banks Bet Big on Non-Banking Businesses

This concentration is worth unpacking rather than treating as coincidence. Kano and Lagos are Nigeria’s two largest commercial centers by transaction volume, meaning they naturally host a disproportionate number of MFBs to begin with—so a higher absolute count of failures is partly a function of a larger population of licensed entities.

But the scale of Kano’s showing, nearly double Lagos’s, in a state with a considerably smaller formal economy, points to something more specific: a cluster of undercapitalized, community-style institutions established during a period of aggressive MFB licensing in Northern Nigeria. Several of the Kano names revoked (Bompai, Minjibir, Shanono, Sumaila, Rimin Gado, and Tofa) share naming conventions tied directly to local government areas, suggesting cooperative-style MFBs that may have lacked the institutional depth to survive tightening prudential standards.

Lagos’s eight failures, by contrast, likely reflect the sheer density and competitiveness of the state’s financial services market, where digital lenders and better-capitalized fintech-MFB hybrids have squeezed out weaker legacy operators—a dynamic that connects to a second, less-noticed dimension of this revocation round.

The tier breakdown: it’s the smallest capital base that took the biggest hit

Unlike previous CBN revocation announcements, the July 1 list—jointly published by the CBN and NDIC—discloses each bank’s license tier alongside its state. That detail sharpens the story considerably:

| License tier | MFBs affected | Share of total |

| Tier 2 (rural, ₦50m minimum capital) | 25 | 54% |

| Tier 1 (urban, ₦200m minimum capital) | 18 | 39% |

| State-licensed (₦1bn minimum capital) | 3 | 7% |

More than half of the revoked licenses (25 of 46) belonged to Tier 2 rural MFBs—the category with the lowest capital floor, at ₦50 million. Only three of the 46 were state-licensed MFBs, the better-capitalized tier requiring ₦1 billion in paid-up capital. In other words, the sub-sector’s smallest, thinnest-margin operators—the ones with the least buffer to absorb loan losses, inflation, or a run of bad governance decisions—bore the overwhelming brunt of this clean-up. That reinforces, with harder data than was previously available, the reading that this is a capital-adequacy story first and a geography story second: Kano’s cluster of failures and the sector-wide Tier 2 skew are two views of the same underlying weakness.

A fintech wrinkle the CBN list didn’t flag but the market noticed

Not every name on the list fits the picture of a moribund community lender. At least five of the 46—Sycamore MFB, NOW NOW Digital MFB, OurPass MFB, Creditville MFB, and Casha MFB—carry recognizable links to Nigeria’s fintech ecosystem, a detail first flagged by Techpoint Africa’s review of the list. Sycamore Group, the digital lender, publicly clarified that the revoked entity was a legacy microfinance license it acquired in 2024 as part of a regulatory transition and that its live operations continue under a separate finance company license obtained since then—meaning the MFB license had become redundant rather than the business having failed.

That distinction matters for how this revocation round should be read. Not all 46 licenses represent institutions that collapsed under CBN scrutiny; some appear to be regulatory house-cleaning of dormant or superseded licenses left behind as fintech-linked lenders migrate to more appropriate license categories. It is a reminder that a bare headline count of “46 banks revoked” can conflate genuine depositor-risk failures with administrative tidying—a distinction worth drawing out for readers rather than collapsing into a single narrative of sector-wide distress.

What this actually means for depositors

NDIC’s maximum deposit insurance coverage for microfinance bank depositors was raised in 2024 from ₦200,000 to ₦2 million per depositor per account — a tenfold increase. NDIC management told the House of Representatives Committee on Insurance and Actuarial Matters earlier this year that this revised coverage now fully protects an estimated 99.27 percent of MFB depositors nationwide, up from roughly 98.76 percent under the old ₦200,000 ceiling.

In practice, the great majority of customers at the 46 closed banks should have their full balances covered.

For the minority with balances above ₦2 million, NDIC’s own track record—most recently demonstrated in the ongoing Heritage Bank liquidation, where it paid a second liquidation dividend of ₦24.63 billion to depositors in January 2026—shows that amounts above the insured threshold are not written off outright but are recovered gradually through liquidation dividends as NDIC realizes the failed institution’s assets and recovers loans.

That process can still take months, but it is a materially different picture than a flat claim that above-threshold depositors simply “face losses.”

NDIC also says technology, chiefly the use of bank verification numbers to automatically locate and credit depositors’ accounts elsewhere, has helped in cutting typical payout timelines for insured sums from years to days in recent resolutions.

Why it matters

For the sector, the revocations reinforce Governor Cardoso’s broader supervisory posture: capital discipline and consolidation are not confined to deposit money banks but extend down to the grassroots tier of Nigeria’s financial architecture. The CBN’s own framing that it “remains committed to promoting a safe, sound, and resilient financial system” echoes the language used around the commercial bank recapitalization drive, suggesting a single, sector-wide philosophy of enforcement rather than a series of unrelated actions.

The risk, as with the commercial bank recapitalization drive, is that tighter capital and compliance thresholds, however necessary for systemic stability, could also shrink the very institutions meant to deepen financial access in underserved communities, particularly in northern Nigeria, where the Kano cluster and the Tier 2 skew together suggest that financial-inclusion gains built on thinly capitalized rural lenders may now be reversing before they have had the chance to consolidate.

At the same time, the fintech-linked names on the list are a useful corrective against reading every revocation as a story of failure: for at least a handful of institutions, this looks more like the regulatory system catching up with license categories that market realities had already outgrown.

Sunday Michael Ogwu is a Nigerian journalist and editor of Pinnacle Daily. He is known for his work in business and economic reporting. He has held editorial roles in prominent Nigerian media outlets, where he has focused on economic policy, financial markets, and developmental issues affecting Nigeria and Africa more broadly.