How China’s $180 billion bet on Africa — from Nigerian railways to Angolan oil — is rewriting the rules of global power, filling the void left by a negligent West, and raising urgent questions about who, ultimately, will pay the price.

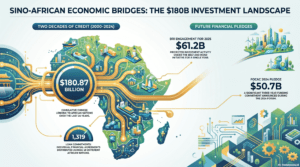

$180.87B Chinese loans to Africa 2000 – 2024; 1,319 loan commitments across 49 nations; $61.2B RI Africa engagement, 2025 alone; $50.7B FOCAC, 2024

three-year pledge

There is a story that does not begin with ideology, or with charity, or even with goodwill. It begins, as most consequential stories do, with a simple, brutal calculation: power abhors a vacuum. And for most of the past two decades, the West has been very good at creating one in Africa.

Into that vacuum – left by disinterested Western donors, aid agencies hobbled by conditions, and creditors who treated the continent as a basket case rather than a boardroom – China walked in, cheque in hand, hard hat at the ready, and a deal on the table that asked only one question: What do you need built?

The answer Africa gave loudly and repeatedly was ‘No’. And China listened.

The Numbers That Changed Everything

The scale of China’s financial penetration of Africa is difficult to overstate. According to the Chinese Loans to Africa (CLA) Database, maintained by Boston University’s Global Development Policy Center – the most comprehensive tracker of its kind – 42 Chinese lenders signed 1,319 loan commitments totalling $180.87 billion with 49 African governments and seven regional institutions between 2000 and 2024. The loans flowed primarily from two institutions: the Export-Import Bank of China (CHEXIM) and the China Development Bank (CDB).

To understand the velocity of this expansion, consider the benchmark: China’s loan commitments grew so fast after 2000 that they exceeded the World Bank’s lending to Africa in most years between 2011 and 2018. The world’s most powerful multilateral development institution, the body designed specifically to finance developing nations, was being outpaced by a single country’s state banks.

Speaking to 51 African heads of state at the FOCAC Summit, Beijing, on September 5, 2024, President Xi Jinping said, “China-Africa relations are currently at their best in their 70-year history.”

READ ALSO:

- Africa Must End Reliance on Foreign Investors – Dangote

- Beyond Oil: Dangote Unveils 20,000MW Power Expansion Plan

At the 9th Forum on China-Africa Cooperation (FOCAC) in September 2024 — described by observers as the largest diplomatic event China has hosted since the Covid-19 pandemic — Xi Jinping put flesh on those numbers. He pledged RMB360 billion ($50.7 billion) in financial support for Africa over the next three years: RMB210 billion in credit lines, RMB80 billion in various forms of assistance, and at least RMB70 billion in investment from Chinese companies. Fifty-one African heads of state turned up. The only absentee was Eswatini, which maintains relations with Taiwan.

But even before that summit’s ink was dry, the BRI’s numbers had surged dramatically. Africa topped China’s Belt and Road Initiative engagement in 2025, reaching a staggering $61.2 billion — a 283 per cent increase over the prior year — with Nigeria and the Republic of Congo leading construction volumes.

The Architecture of Influence: How the Model Works

China’s engagement model in Africa is not a single strategy — it is a layered system. At its foundation is infrastructure: roads, railways, ports, dams, airports, and broadband networks. These are financed by state-controlled development banks at concessional rates, built by Chinese state-owned construction companies, and staffed at senior technical levels by Chinese workers. The host country receives a tangible asset. China receives strategic access, trade leverage, and, in many cases, a collateral claim on future revenue or natural resources.

Analysts at Boston University describe two tracks of engagement: an electrification track — general support for power plants and transmission infrastructure — and an extraction track, covering the exploration, extraction, and export of primary energy commodities and transition minerals to China. Both tracks serve China’s domestic industrial needs while simultaneously building long-term dependency relationships.

The formula is reinforced by Confucius Institutes — China has now established 74 across 47 African countries — that ensure cultural and linguistic osmosis alongside economic ties. In Nigeria alone, the proportion of private Chinese enterprises has reached 95 per cent of all Chinese businesses, a sign that the relationship has deepened well beyond the purely state-to-state level.

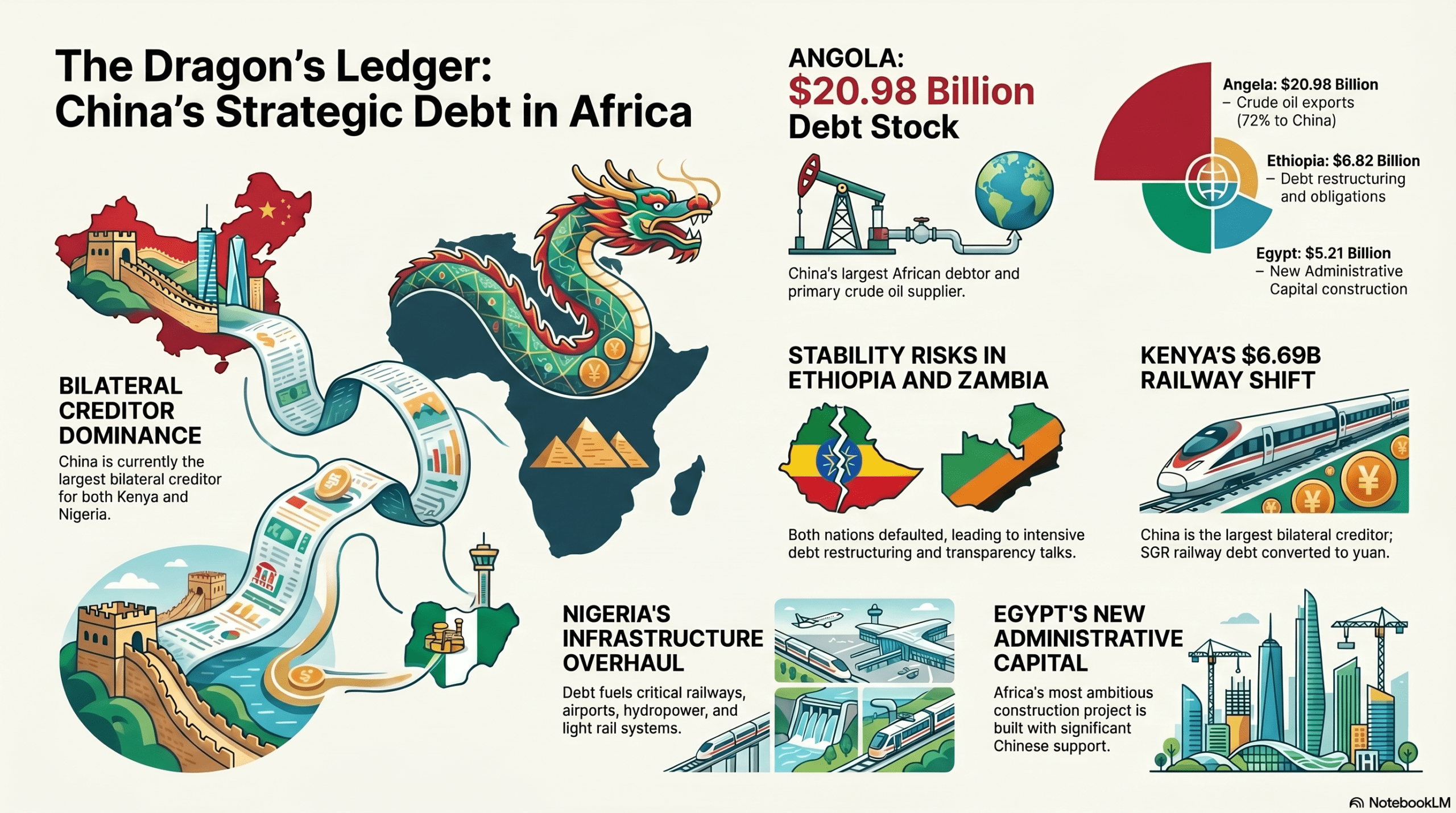

China’s Largest Debtors in Africa (2022 Debt Stock)

- Angola ($20.98 billion) — also China’s largest African crude oil supplier; 72% of oil exports to China in 2021

- Ethiopia ($6.82 billion) — defaulted; China undertook its third debt restructuring of Ethiopian obligations

- Kenya: $6.69 billion — China is Kenya’s largest bilateral creditor; SGR railway will be converted to yuan in 2025

- Zambia ($5.73 billion) — defaulted; Chinese debt transparency became a flashpoint in restructuring talks

- Egypt: $5.21 billion — Africa’s most ambitious construction site, the New Administrative Capital, built with Chinese support

- Nigeria: $5.16 billion (end of 2023) — China is Nigeria’s largest bilateral creditor; railways, airports, hydropower, light rail

Nigeria: Africa’s Giant Becomes China’s Biggest Canvas

No country illustrates the paradoxes and possibilities of Chinese investment in Africa more vividly than Nigeria. The continent’s most populous nation, largest economy by GDP, and one of its most dysfunctional states — chronically under-infrastructured, oil-dependent, and serially betrayed by successive governments — found in China a partner that the West had consistently failed to be.

Nigeria and China formalised their strategic partnership with a memorandum of understanding in 2006 — the first such deal China signed with any African country — which included an oil-for-infrastructure arrangement giving Chinese companies preferential access to oil-processing licences.

Presidential visits drove the financial pipeline: President Goodluck Jonathan’s visit to Beijing in 2013 unlocked a $3 billion loan for airport expansions in Lagos, Kano, Abuja, and Port Harcourt. President Buhari’s 2016 trip yielded a further offer of $6 billion in infrastructural loans. By the end of 2023, Nigeria’s debt to China had reached $5.16 billion, making China Nigeria’s largest bilateral creditor.

Chinese loans part-funded an extraordinary list of projects under the Belt and Road Initiative: the Abuja-Kaduna Railway, the Lagos-Ibadan Railway, the Abuja Light Rail, the Zungeru Hydroelectric Power Project ($984 million), the NIGCOMSAT communications satellite, the Lekki Deep Sea Port, the four international airport terminals (Abuja, Lagos, Kano, and Port Harcourt), and the Greater Abuja Water Supply Project. In 2025, Nigeria’s construction volume under BRI surged to a staggering $24.6 billion, making it the single largest BRI construction recipient in the world in that period.

READ ALSO:

- U.S. Proposes Critical Minerals Trade Bloc to Counter China’s Influence

- China Condemns U.S. Trade Probe Ahead of Key Paris Negotiations

Yet the relationship is not without its shadows. The $823 million Abuja Light Rail — financed by China’s Export-Import Bank and celebrated as West Africa’s first — was shuttered in March 2020 and remained non-operational for years, even as Nigeria continued to service a $500 million loan at $50 million per year. The trains, it turned out, ran where the city’s planners imagined people should live rather than where they actually do.

Speaking on this development, Nasir El-Rufai, former FCT minister and governor of Kaduna State, who signed the original Abuja light rail contract, said, “The line basically avoided where people are, where people live, and where people go.”

Meanwhile, Nigeria’s House of Representatives voted unanimously in May 2020 to probe Chinese loans – a decision made despite a direct plea from the then-transport minister, Rotimi Amaechi, who asked lawmakers to “look the other way” lest the scrutiny frustrate future Chinese lending. The opacity of those loans — Chinese EXIM Bank guidelines require that Chinese firms be selected as contractors and that 50 per cent of project equipment be sourced from China — has fuelled persistent concerns about sovereignty and value for money.

The Western Retreat: Aid in Freefall

To understand why Africa opened its doors to China so comprehensively, one must understand what the West’s door looked like from the African side: half-closed, conditional, and perpetually shrinking.

The history is long and unglamorous. During Angola’s devastating civil war — which killed more than 500,000 people and lasted 30 years — Western interest was consumed by the post-9/11 “War on Terror” in Afghanistan and Iraq. Angola turned to China, which agreed to provide infrastructure investment in return for oil. The Djibouti lesson is starker still: a nation of one million people with limited natural resources received an estimated $41.4 billion in Chinese infrastructure investment — a port, a railway, and a water pipeline — and subsequently gave China its first overseas military base, located just kilometres from a US naval base.

More recently, the Western retreat has accelerated dramatically. France, Germany, the United Kingdom, and the United States all cut their aid budgets simultaneously in 2024–2025 — the first time in decades that all four have pulled back at the same time. Sub-Saharan Africa sits squarely in the bullseye.

The Aid Collapse: Key Figures

France announced a €742 million (12.5%) cut to its development aid in February 2024 — its largest in a decade — followed swiftly by a further 37% cut of €2.1 billion in 2025. USAID, once the world’s largest aid agency, spent $12 billion in sub-Saharan Africa in 2024 before being effectively dismantled under the Trump administration. Countries including Ethiopia, Nigeria, South Sudan, and the Democratic Republic of Congo — among Africa’s largest historical aid recipients — now face steep declines in support across health, food security, and humanitarian programmes.

The consequences have been concrete and cruel. PEPFAR — the US President’s Emergency Plan for AIDS Relief — which supports HIV treatment and prevention in more than 20 African countries, has faced severe cuts. South Africa, which has more people living with HIV than any other country, lost $439.5 million in one fiscal year. Malaria programmes, polio and rotavirus vaccination campaigns, and community health infrastructure have all been slashed.

Speaking on the termination of US health aid programmes, Professor Salim Abdool Karim, a South African epidemiologist, said, “The termination was deliberately brutal, deliberately disruptive, and chaotic.”

Against this backdrop, China’s message at FOCAC 2024 — delivered by Xi Jinping in the cavernous Great Hall of the People before more than 50 African leaders — carried the unmistakable weight of contrast. Beijing positioning itself as a “fellow developing country” against the West’s “colonialist past” is rhetoric, certainly. But rhetoric lands very differently when your opponent has just cancelled the malaria programme.

The Exploitation Debate: Dragon or Deliverer?

The Western narrative about China’s role in Africa has crystallised around the concept of “debt-trap diplomacy” — the idea that China deliberately loads countries with unrepayable debt, then extracts strategic concessions when they default. The Sri Lankan Hambantota Port precedent—where a 99-year lease was handed to China after a default—became the cautionary parable repeated in think tanks from Washington to Brussels.

But the picture, examined closely, is more complex. The World Bank itself reported that as of 2022, Chinese debt constituted only 13 per cent of Africa’s total external debt — roughly equivalent to what Africa owed the World Bank and well below the 28 per cent owed to private bondholders. Zambia, Ghana, and Ethiopia — the three African countries that defaulted in recent years — were all among China’s top 10 borrowers, but their collapses were shaped by multiple creditors, including Western private lenders who charge significantly higher interest rates.

China also has a documented history of restructuring rather than seizing. Over the past decade, China restructured or forgave loans in 84 cases without taking possession of assets, including three restructurings of Ethiopian debt and ongoing negotiations with Zambia. In October 2025, Kenya converted an estimated $3.5 billion of its Standard Gauge Railway debt from dollars to yuan — a move designed to lower interest costs, not to deepen dependence.

Responding to debt-trap allegations, Ethiopia’s ambassador to China, Teshome Toga Chanaka, said, “A partnership that does not benefit both will not last long.”

Yet this defence has its limits. The opacity of Chinese loan agreements is real, not rhetorical. Nigeria’s National Assembly needed to threaten a parliamentary probe simply to access the terms of loans already committed in their name. In Zambia’s debt restructuring talks, China initially refused to join multinational negotiations, negotiating separately and insisting on confidentiality clauses that prevented disclosure to other creditors – a conduct described by financial analysts as fundamentally incompatible with collective debt management norms that Western creditors had long respected.

According to a BusinessDay Nigeria article citing financial analysts on China’s conduct in Zambia’s debt restructuring, 2023, it was noted that “China didn’t play by those rules.” It refused at first to even join in multinational talks, negotiating separately and insisting on confidentiality.”

The African criticism of Chinese exploitation is also not merely academic. Pan-African civil society leader Kumi Naidoo, speaking at the All-African Movement Assembly in Accra in 2024, articulated a frustration directed not solely at China but at all external actors:

He said, “We are not asking the West to give us charity. We are demanding reparative justice in the form of meaningful and effective aid.”

The frustration cuts in every direction. China is criticised for using Chinese labour instead of local workers, for extracting raw materials without value addition, and for flooding African markets with cheap manufactured goods — China’s steel exports to Africa rose 34 per cent by volume in 2024 and a further 34 per cent in the first nine months of 2025. Western creditors are criticised for conditions, delays, and abandonment. And African governments are criticised for mortgaging national assets in deals that were signed, in many cases, with a handshake at a presidential banquet.

A Strategic Recalibration

China, to its credit, appears to be reading the room. The era of massive sovereign lending — which peaked at $28.2 billion in 2016 — has given way to a more selective, diversified engagement model. In 2024, Chinese loan commitments to Africa fell to just $2.1 billion, with only five countries (Angola, Kenya, the DRC, Senegal, and Egypt) receiving any new lending. The emphasis has shifted toward foreign direct investment, RMB-denominated loans, equity partnerships, and private sector engagement.

The new toolkit includes “Panda bonds” — African sovereign bonds issued in China’s capital markets — with Egypt already having issued one backed by the Asian Infrastructure Investment Bank and the African Development Bank. Renewable energy projects are increasingly funded through FDI rather than sovereign debt. In Nigeria, hydrogen and electric vehicle battery projects are now at the frontier of Chinese investment, alongside the massive oil and gas construction that dominated the 2025 BRI figures.

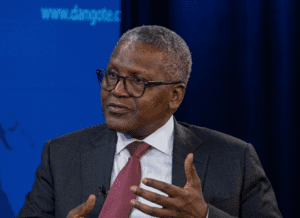

Speaking emphatically on this development at a business programme, Africa’s richest man, Aliko Dangote, said, “China really has dominated business in Africa because of the absence of the others. “They are dominating the landscape.

“And obviously, Africans, even our own governments, don’t joke with China because China puts their balance sheet on the table. They give you a supplies credit backed by their insurance company, which is called SinoSure. SinoSure has invested about $1.2 trillion in supporting their companies to go abroad and sell their technology and sell their equipment and giving you a credit of four or five years.”

The Question That Remains

Africa boasts 30 per cent of the world’s mineral reserves. It holds the lithium the world’s electric vehicles need. It sits on the cobalt that powers our smartphones. Its population, projected to reach 2.5 billion by 2050, represents the largest untapped consumer market in human history. And it possesses, in nation after nation, a yawning infrastructure deficit — roads unbuilt, power ungenerated, ports undeepened, water undelivered.

China saw all of this. The West, to varying degrees, either did not see it or saw it and decided not to act. The divergence of that vision — and of the willingness to show up — is the central geopolitical story of the 21st century. It is not a simple story of dragon versus saint. China has built railways that move goods and airports that move people; it has also written loan terms that moved sovereignty. The West has funded vaccines and preached democracy; it has also cut off those same vaccines when the geopolitical winds changed.

What is beyond dispute, as the data assembled here shows, is that Africa is no longer merely the subject of this contest. African finance ministers are demanding yuan-denominated loans to reduce dollar exposure. African presidents are attending Chinese summits and Western summits and increasingly leaving Beijing with more to show for it. And African civil society is growing louder in its insistence that the continent’s resources, its debt, and its future belong to its people — not to the interests, Eastern or Western, that circle its vast potential.

The dragon is in Africa. It has been for a generation. The question now is whether Africa will learn, in time, to hold the leash.

Sunday Michael Ogwu is a Nigerian journalist and editor of Pinnacle Daily. He is known for his work in business and economic reporting. He has held editorial roles in prominent Nigerian media outlets, where he has focused on economic policy, financial markets, and developmental issues affecting Nigeria and Africa more broadly.